Stocks

Stocks finished the last day of February in the red, which was indicative of a month that saw losses for the three U.S. equity benchmarks.

For the month of February, the stock market’s three major indices performed as follows:

Dow -4.2%

S&P 500 -2.6%

Nasdaq -1.1%

Inflation

Inflation took an unexpected turn through January, disappointing what was hoped to be a deflationary trend.

For the month, the Consumer Price Index (CPI) increased 0.5% month-over-month, rising 6.4% on an annual basis.

That outpaced forecasts, which had anticipated that 0.5% monthly increase but only a 6.2% annual CPI increase.

Furthermore, December’s inflation numbers were upwardly revised to a 0.1% increase for the last month of 2022, not the 0.1% decrease that was previously reported.

When looking at Core CPI, which doesn’t factor in energy and food costs, inflation rose 5.6% year-over-year and 0.4% from the previous month, both surpassing estimates as well.

Higher-than-expected inflation led to a sigh of disappointment from investors and Wall Street, who now foresee more Fed rate increases.

February’s pace of inflation will be revealed with the next CPI report on March 14th.

Interest Rates and the Fed

At its February meeting, the fed raised its target range for the funds rate to 4.5%-4.75%, a 25-bps increase. That marked the second straight meeting of pulling back the size of rate increases, although still setting borrowing costs at the highest level since 2007.

However, hotter-than-expected inflation data is sure to leave the fed thinking hard about accelerating rate increases for its next meeting on March 21-22.

With disinflation hopes seemingly off the table, most analysts expect the fed to push rates higher and keep them elevated longer in search of their ideal target of 2% inflation.

Jobs and unemployment

Total non-farm payrolls jumped by 517,7000 in January, as reported by the U.S. Labor Department’s February 3rd report.

Adding an additional half a million jobs shattered the forecast of 188,000 new payrolls, an astounding difference.

The unemployment rate also fell to 3.4%, down from predictions of 3.6% and little changed from the previous month’s 3.5% unemployment rate.

Leisure and hospitality added 128,000 jobs in January, professional and business services added 82,000, government employment increased by 74,000 jobs, and healthcare gained 58,000 new employees.

The next employment data is set to be released on Friday, March 10th.

Gross Domestic Product

According to second estimates released February 23rd, our real gross domestic product (GDP) rose 2.7 percent in the fourth quarter of 2022. That’s a significant decrease of 0.2 compared to the initial estimate of 2.9 percent economic growth for Q4.

That also follows a Q3 3.2 percent increase in GDP.

The biggest contributor to the GDP downward revision was new data from consumer spending, which fell more than expected.

Consumer Spending

U.S. consumer spending rose 1.8% in January, the largest gain in nearly two years as consumers faced higher prices due to inflation – but solid wage growth and a halcyon job market.

Consumer spending accounts for more than two-thirds of U.S. economic activity as measured by GDP, and January’s nearly 2% increase in spending was the largest bump since March 2021.

Household debt

Even amid stubborn inflation and a white-hot job market, total household debt is rising at alarming levels. In fact, personal debt hit a record $16.9 trillion in Q4 2022 and has just kept rising so far in 2023.

The Q4 increase was also notable because it represented a 2.4% increase from the previous quarter or $394 billion in only three months. Much of that can be attributed to rising mortgage debt, but credit card balances swelled by 6.6%, or $986 billion, during Q4 as well.

Year-over-year, credit card balances grew by 15.2%, the highest quarterly increase on record, according to New York Fed data which goes back to 1999.

Housing Market

The fed’s campaign of hiking their benchmark interest rates to dampen inflation has caused significant collateral damage in the U.S. housing market. As rates basically doubled from the end of 2021 to Q4 2022, homebuyers and those looking to refinance suffered unprecedented sticker shock.

But by the end of January 2023, there was far more optimism as mortgage rates settled closer to the important 6% barrier. Many predicted a healthier – if not normalized – spring and summer homebuying season.

However, those hopes were dashed as the fed’s continued rate increases and worse-than-expected inflation data drove up rates once again, dangerously close to approaching the 7% mark at the time of this writing.

While home prices have not plummeted (they are still positive year-over-year after a huge head start of home appreciation through Q3 2022), they are falling – which most just see as a healthy correction.

But the bigger problem is home sales volume. Buyers are just not buying, facing an affordability crunch not seen since 2007, and sellers are reluctant to put their homes on the market and move, when they’ll face the same conundrum.

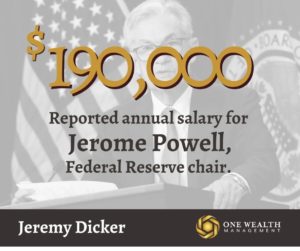

Does the Fed Chairman deserve a raise?

In a recent interview, Fed chair Jerome Powell, arguably one of the most influential figures in America’s economy, disclosed that he makes about $190,000 per year.

He also said that he feels that number is fair.

Per Fortune magazine: “Investors the world over hang on the Federal Reserve chair’s every word and his speeches are parsed for the slightest directional hint on U.S. interest rate policy—because his institution essentially decides on what money itself costs. And yet despite Powell’s enormous influence, he earns a take-home pay that America’s chief executives would scoff at.

“It’s around $190,000 I believe,” said Powell, who joined the fed’s board of governors in 2012 before rising to become head of the central bank six years later. “If we have family expenses that exceed my salary, then we have to sell an asset,” he added.”

Notable Quote

“I have yet to see a time when it made sense to make a long-term bet against America.”

– Warren Buffett, in his 2022 Berkshire shareholder letter