Stock Market

While the stock market often sees a September swoon, last month bucked the trend with a record-breaking performance. Investors embraced remarks by Federal Reserve Chair Jerome Powell on the ultimate trading day of the month, leading Wall Street to fresh records and a robust quarter.

For the month of September, the stock market’s three major indices performed as follows:

The Dow +1.9%

S&P 500 + 2%

Nasdaq +2.7%

For Q3, the big three indices closed the quarter as follows:

The Dow + 8.2%

S&P 500 +5.4%

Nasdaq +3%

For the S&P 500, it was its best year-to-date performance at the end of September since 1997 and its best quarter since Q4 of 2021.

Inflation

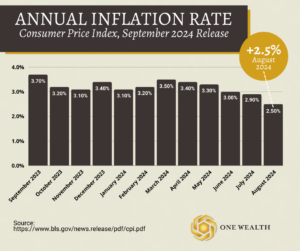

On a seasonally adjusted basis, the Consumer Price Index rose 0.2% in August according to the U.S. Bureau of Labor Statistics, the same increase inflation saw in July.

Spanning twelve months, annual all-items inflation rose by 2.5% on a seasonally adjusted basis. That level of price increases was just 0.1% lower than Wall Street’s expectations but also the lowest in more than three years since February 2021.

However, core CPI – stripping away volatile food and energy costs – rose 0.3% in August, just pushing past estimates. On a 12-month basis, core inflation drove higher at 3.2%, with elevated shelter costs (0.5% in August) the main culprit.

The Core Personal Consumption Expenditure (PCE) Price Index, a key inflation measure excluding volatile components like food and energy, rose by 0.1% in August, following a 0.2% increase in July. This was in line with economist forecasts and reflects a slight deceleration in inflationary pressures. On a 12-month basis, core PCE inflation advanced to 2.7%, up from 2.6% in July, though overall PCE inflation increased by 2.2%, down from 2.5% the previous month.

Jobs and Unemployment

Total nonfarm payroll employment increased by 142,000 in August according to the U.S. Bureau of Labor Statistics, notably lower than the 165,000 new hires projected by economists. August marked the fifth month of new payroll decreases, with job openings falling to the lowest level since January 2021. The most significant job gains came in health care and construction.

While new payrolls underwhelmed, the unemployment rate did fall to 4.2% from 4.3% in July.

Based on the recent data, economist Paul Ashworth noted in his August jobs report that the labor market “[is] still consistent with an economy experiencing a soft landing rather than plummeting into recession.”

GDP

The U.S. economy grew at a 3% annualized rate in the second quarter, surpassing Wall Street’s expectations. The Bureau of Economic Analysis’ third estimate confirmed the unchanged 3% growth, slightly above economists’ forecast of 2.9%. This marks a significant increase from the 1.4% growth in the first quarter. The Atlanta Fed’s GDPNow tracker currently projects a 2.9% annualized growth rate for the U.S. economy.

The Strong Dollar: Impact & Implications

The strength of the U.S. dollar has wide-reaching effects on global trade, economic stability, and investment strategies. A strong dollar benefits U.S. consumers and importers by making foreign goods cheaper, but it can hurt exporters by making American products more expensive abroad. Foreign companies selling to the U.S. may benefit from increased demand, though their debt can become more costly if their local currency weakens against the dollar.

Key economic indicators like interest rates, inflation, and growth influence the dollar’s strength. High U.S. interest rates attract foreign capital, boosting the dollar and curbing inflation, while its status as the world’s reserve currency allows the U.S. to borrow more cheaply and manage trade deficits.

In the long term, the dollar’s strength will depend on economic policies and global conditions. A high interest rate environment may sustain the dollar’s value, but global economic recovery or alternative currencies could weaken its dominance.

The Fed and Rates

At its September 17-18 meeting, the Federal Reserve enacted its first interest rate cut since the onset of the Covid pandemic, reducing the benchmark rate by half a percentage point. The Federal Open Market Committee (FOMC) lowered the federal funds rate to a range of 4.75% to 5%, exceeding the more modest cuts initially expected by market participants. This marks the first non-emergency half-point rate cut since the 2008 financial crisis, signaling the Fed’s urgency in addressing the softening economic landscape.

In addition to the immediate reduction, the Fed signaled that more rate cuts are on the horizon, projecting an additional 50 basis points in reductions by the end of the year. The “dot plot” of individual officials’ forecasts suggests that by the end of 2025, the benchmark rate will be lowered by a full percentage point, with a further half-point reduction expected in 2026.

The post-meeting statement emphasized the Fed’s growing confidence that inflation is approaching its 2% target, with employment and inflation objectives now better balanced.

Real Estate and Mortgage

Lower mortgage rates are helping to bring much-needed stability to the housing market, with the average 30-year home loan rate now in the 6.2% range, the lowest point in more than two years.

While we are no longer in the era of sub-3% loans, today’s rates have fallen below the 52-year historical average of 7.72%. With the Federal Reserve starting a cycle of lowering interest rates, there’s renewed optimism for those looking to purchase or refinance, providing an opportunity for more favorable conditions ahead.

While home prices continue to rise—up 5.2% year-over-year as of June, according to the Freddie Mac House Price Index—the inflation-adjusted growth has been more moderate than nominal rates suggest. The dramatic price increases seen during the pandemic have slowed down, and in some areas, prices have even reversed. This signals a return to a more balanced and sustainable housing market.

Notable Quote

“The idea that a bell rings to signal when to get into or out of the stock market is simply not credible. After nearly fifty years in this business, I don’t know anybody who has done it successfully and consistently. I don’t even know anybody who knows anybody who has.”

– Jack Bogle