Stock Market

June saw the second straight month of significant gains on Wall Street, finishing up a strong second quarter.

For the month, the stock market’s three major indices performed as follows:

S&P 500 5%

The Dow 4.3%

Nasdaq 6.6%

Recent market sentiment has improved, driven by a more stable geopolitical environment following a cease-fire between Israel and Iran, renewed hopes for U.S. trade deals that could reduce tariffs, and growing optimism that the Federal Reserve may lower interest rates in the near future.

For Q2 2025, the S&P 500 added more than 10%, the Nasdaq rose nearly 18%, and the Dow climbed almost 5%.

Sources:

https://www.investopedia.com/dow-jones-today-06302025-11763396

https://www.cnbc.com/2025/06/29/stock-market-today-live-updateshtml.html

Inflation

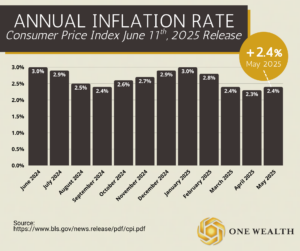

Consumer prices rose 0.1% in May, slightly below expectations, bringing the annual inflation rate to 2.4%, according to the U.S. Bureau of Labor Statistics. Shelter and food costs each rose 0.3%, while energy prices dropped 1.0% due to falling gas prices. Core inflation, excluding food and energy, also rose 0.1%, with increases in medical care, insurance, and personal care. Over the past year, food prices are up 2.9%, core inflation is up 2.8%, and energy is down 3.5%.

Markets responded calmly, with the S&P 500 up 0.1%, staying near record highs. Treasury yields dipped as inflation came in below the expected 2.5%. While Trump-era tariffs haven’t yet driven prices higher, economists caution their effects may still emerge. Trade talks between the U.S. and China offered modest progress, with hopes for a broader deal boosting investor optimism. Tesla gained 1.4% after Elon Musk walked back earlier remarks, while Chewy fell 11.8% after disappointing earnings.

Sources:

https://www.bls.gov/news.release/pdf/cpi.pdf

https://www.washingtonpost.com/business/2025/06/11/stock-markets-china-trump-tariffs/14306d5c-467d-11f0-9210-87ee82efcc80_story.html

Jobs & Unemployment

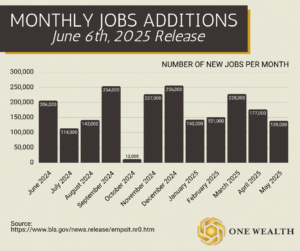

U.S. job growth continued at a modest pace in May, with nonfarm payrolls rising by 139,000, according to the Bureau of Labor Statistics. However, downward revisions to prior months—95,000 fewer jobs combined in March and April—bring the three-month average job gain down to 135,000. The unemployment rate held steady at 4.2% for the third straight month, with 7.2 million people unemployed and 625,000 individuals leaving the labor force, contributing to a slight decline in the labor force participation rate to 62.4%. Employment grew in sectors like health care, leisure and hospitality, and social assistance, while federal government jobs declined.

Despite the steady unemployment rate, cracks in the labor market are beginning to show. Short-term unemployment (under 5 weeks) increased by 264,000 to 2.5 million, even as long-term unemployment declined to 1.5 million. The employment-population ratio dipped to 59.7%. Economists suggest the slowdown may be driven by uncertainty over the Trump administration’s shifting tariff policies and government spending plans, which have made it difficult for businesses to plan hiring. Still, solid wage growth has helped maintain economic stability, potentially giving the Federal Reserve room to hold off on further interest rate cuts.

Sources:

https://www.bls.gov/news.release/pdf/empsit.pdf

https://www.reuters.com/world/us/us-job-growth-slows-may-unemployment-rate-steady-42-2025-06-06/

GDP

The U.S. economy contracted slightly in Q1 2025, with real gross domestic product (GDP) declining at an annual rate of 0.5%, following a 2.4% gain in Q4 2024, according to the Bureau of Economic Analysis. This downturn was driven primarily by a surge in imports and reduced government spending, though these were partially offset by increases in consumer spending and private investment. The GDP revision downward by 0.3 percentage points from the previous estimate reflected weaker-than-expected consumer spending and exports. Meanwhile, real final sales to private domestic purchasers rose 1.9%, though that figure was revised down 0.6 percentage points.

Industry-specific data showed a mixed picture: real value added fell 2.8% in goods-producing industries and 0.3% in services-producing industries, while government sector value added rose 2.0%. Real gross output increased 0.6%, buoyed by a 1.1% rise in services despite declines of 0.6% in both goods and government output.

Sources:

https://edition.cnn.com/2025/06/26/economy/us-gdp-q1-final

https://www.bea.gov/index.php/news/2025/gross-domestic-product-1st-quarter-2025-third-estimate-gdp-industry-and-corporate-profits

Portfolio Diversification in a Shifting Market

With traditional stock and bond markets facing mounting volatility—driven by geopolitical risks, tariff uncertainties, and looming economic slowdowns—investors are turning their attention to alternative investments. Assets such as private equity, private credit, digital assets, and real estate have not only provided comparable or superior returns to public equities over the past decade, but they also tend to be less reactive to daily market sentiment. For long-term investors comfortable with reduced liquidity, this can mean a more stable path to wealth accumulation.

Three key themes are driving the shift:

1) Real estate—especially alternative property types like student housing, self-storage, and senior living—is attracting younger investors and showing strong performance.

2) AI and infrastructure—the rollout of AI will demand over $1 trillion in capital, much of it sourced privately, offering attractive opportunities for investors.

3) Crypto and deregulation—regulatory momentum is building for the integration of digital assets into mainstream portfolios, with stablecoins and blockchain technologies providing new options for inflation hedging and security.

Looking ahead, retirement portfolios like 401(k)s may soon allocate 10–20% to private assets, following the lead of institutions and major providers like Empower. Diversification is no longer just a buzzword—it’s an essential strategy for navigating an uncertain financial future.

Source:

https://www.crystalfunds.com/insights/portfolio-diversification-strategies-uneasy-times

Real Estate and Mortgage

The U.S. housing market is finally showing signs of normalization after years of volatility. While mortgage rates remain stubbornly in the mid-to-high 6% range, there are some positive developments that point to a more balanced market:

Inventory is Growing – Homes for sale increased by 31.5% year-over-year in May, reaching the highest levels since the pandemic began.

Price Reductions Are Common – Nearly 1 in 5 homes had listing price cuts in May, the most since 2016, continuing a five-month trend.

Homes Are Taking Longer to Sell – Average time on market rose to 51 days, up six days from last year.

Credit Is Loosening – Lenders are easing mortgage requirements, offering more loan options as credit availability reaches its highest point since August 2022.

While challenges like high mortgage rates persist, more inventory, slower sales, and easier credit signal a cooling and more balanced real estate market.

Notable Quote

“The real key to success in the markets is not intellect but emotional discipline.”

– Daniel Kahneman