Stock Market

What a year it’s been already – and it’s only January! To some, the past month has felt like far more than 31 days on Wall Street, and for good reason through a headline-filled, volatile start to 2026.

Stocks pulled back on Friday, the last trading day of the month, as technology shares continued to struggle, even as investors generally welcomed President Donald Trump’s selection of Kevin Warsh to lead the Federal Reserve.

Despite Friday’s losses and the volatility that defined much of the month, the major indexes managed to finish January in positive territory.

- S&P 500 +1.4%

- The DOW +1.7%

- Nasdaq Composite +0.9%

That said, the gains were largely front-loaded. The Dow has now declined for three consecutive weeks, marking its longest weekly losing streak since December 2024.

Looking at the bigger picture, however, the trend remains constructive. January’s advance marked the Dow’s ninth straight positive month, its longest monthly winning streak since 2018.

Sources:

https://www.barrons.com/articles/stock-market-today-january-fed-warsh-706eaa50

https://www.cnbc.com/2026/01/29/stock-market-today-live-updates.html

Inflation

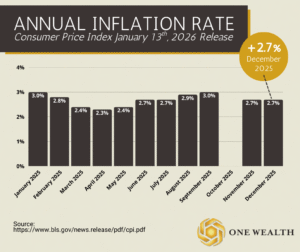

U.S. inflation ended the year showing signs of moderation, though price pressures remain uneven across the economy. According to the U.S. Bureau of Labor Statistics, the Consumer Price Index for All Urban Consumers (CPI-U) increased 0.3% in December on a seasonally adjusted basis, bringing the 12-month inflation rate to 2.7%, unchanged from November.

This final CPI report of 2025 reflects a year in which inflation gradually eased after briefly rising to 3% in September, supported by slower price increases in areas such as gasoline and new vehicles.

December’s monthly increase was driven primarily by higher shelter and food costs. The shelter index rose 0.4%, making it the largest contributor to the overall increase, while food prices climbed 0.7%, with both food at home and food away from home rising at the same pace. Energy prices also increased 0.3% for the month.

Excluding food and energy, core inflation rose 0.2% in December and 2.6% over the past 12 months. Categories such as recreation, airline fares, medical care, apparel, personal care, and education saw price increases, while indexes for communication, used cars and trucks, and household furnishings declined.

On a year-over-year basis, food prices increased 3.1% and energy prices rose 2.3%, contributing to continued pressure on household budgets, particularly for groceries and utilities.

Sources:

https://www.bls.gov/news.release/cpi.nr0.htm

https://www.usatoday.com/story/money/2026/01/13/annual-inflation-cpi-december-report/88133586007/

GDP

U.S. real gross domestic product (GDP) grew at a 4.4% annualized rate in the third quarter of 2025, according to an updated estimate from the Bureau of Economic Analysis, accelerating from 3.8% growth in the second quarter.

The revised figure was 0.1 percentage point higher than the initial estimate, largely due to stronger exports and business investment, partially offset by a downward revision to consumer spending. Growth in the quarter was supported by increases in consumer spending, exports, government spending, and investment, while imports declined.

Sources:

https://www.bea.gov/news/2026/gross-domestic-product-3rd-quarter-2025-updated-estimate-gdp-industry-and-corporate

https://www.monitordaily.com/u-s-economy-grew-faster-than-expected-in-third-quarter-as-investment-and-exports-strengthened/

Jobs & Unemployment

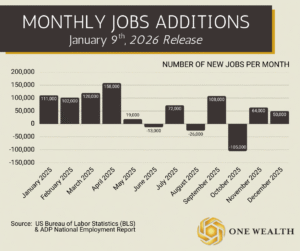

December’s U.S. employment report showed continued job growth, though at a slower pace. According to the U.S. Bureau of Labor Statistics, nonfarm payrolls increased by 50,000 jobs, while the unemployment rate remained at 4.4%, with 7.5 million people unemployed.

Hiring was concentrated in leisure and hospitality, food services, health care, and social assistance, while retail trade, construction, and manufacturing saw job losses.

After revisions, October and November payrolls were reduced by 76,000 jobs, and total payroll growth for 2025 reached 584,000, the weakest annual increase since 2020. Wages rose 0.3% in December, bringing year-over-year wage growth to 3.8%, above inflation.

Sources:

https://www.bls.gov/news.release/pdf/empsit.pdf

https://www.bloomberg.com/news/live-blog/2026-01-09/us-employment-report-for-december

Just Don’t Do It?

In March of 2025, Nike’s stock hit a seven-year low after annual revenue fell 16%, wiping $184 billion off its market cap from its all-time high. A key driver was its strategic shift away from third-party retailers like Dick’s and Foot Locker toward direct-to-consumer channels such as Nike stores and the SNKRS app. This move opened the door for competitors, while Nike leaned heavily on legacy products like Air Jordans, Dunks, and Air Force 1s instead of accelerating new product innovation.

Nike’s recent performance offers a clear case study in how dominant consumer brands can lose ground when they prioritize scale over innovation and customer focus.

As Nike focused on being everywhere at once, emerging competitors doubled down on excelling in targeted segments. On Cloud expanded from 0.22% global market share to 2% by 2024, delivering consistent double-digit growth, while Hoka posted 20% year-over-year revenue growth and now commands 50% of running specialty sales. These brands succeeded by prioritizing specialty retail, performance-driven design, and community-based marketing—areas where Nike’s broad, top-down approach fell short.

Nike’s story underscores a broader shift in consumer markets: today’s winners are defined less by reach and more by focus, product excellence, and authentic brand connection. The company’s recent challenges show how even the most iconic global brands can lose momentum if they stop leading with innovation and rely too heavily on legacy products, mass distribution, and past success.

Sources:

https://www.crystalfunds.com/insights/the-battle-of-the-consumer-brands

https://www.nike.com/es/

Real Estate & Mortgage Market

A year-end review shows the U.S. housing market moved closer to balance in 2025, with inventory rising faster than expected, price growth moderating, and sales inching higher – setting the stage for a potentially steadier 2026. Active listings climbed sharply year over year, reaching approximately 1.3 million by November 2025, as more homeowners listed properties despite holding historically low mortgage rates. Economists expect inventory growth to continue into 2026 across both new and existing homes.

Home price growth also cooled as predicted. Annual price appreciation slowed to 2.4% by November, with median home prices holding in a relatively tight $375,000–$395,000 range for much of the year. Existing-home sales showed gradual improvement, running about 2% higher through October compared to the prior year, though still well below pre-pandemic levels as many homeowners remained “locked in” to lower rates.

Source:

Notable Quote:

“Markets reward patience, discipline, and a clear strategy – not constant handling driven by headlines or emotion. A well-built portfolio doesn’t need to be touched every time the news cycle changes. The goal isn’t inactivity; it’s intentional action guided by a plan – not impulse.”

– Warren Buffett