Stock Market

U.S. stocks delivered another banner year in 2025, supported by resilient corporate earnings, continued enthusiasm around AI, and growing optimism that the Federal Reserve could begin cutting interest rates.

In fact, the U.S. stock market just achieved something remarkably rare: three consecutive years of double-digit gains – an outcome that has occurred only six times since the 1940s.

For the year, the market’s three major indices performed as follows:

- S&P 500: +16.39%

(following gains of 23% in 2024 and 24% in 2023)

- Dow Jones Industrial Average: +12.97%

- Nasdaq Composite: +20.36%

Historically, a three-peat of double-digit annual gains is uncommon. Prior to this year, it had happened only five times. Of those instances, two extended into a fourth consecutive year of double-digit gains, while one – during the 1990s – stretched into a five-year streak.

Artificial intelligence remained one of the dominant investment themes this year, helping propel the tech-heavy Nasdaq to the strongest performance among the three major indexes for the third straight year.

Market performance was mixed for the month of December:

- S&P 500: -0.1%

- Dow Jones Industrial Average: +0.7%

- Nasdaq Composite: -0.5%

Despite modest December results for some indexes, the Dow Jones Industrial Average notched its eighth consecutive monthly gain, marking its longest winning streak since 2018.

Sources:

https://edition.cnn.com/2025/12/31/investing/year-gains-us-stock-market

https://www.cnbc.com/2025/12/30/stock-market-today-live-updates.html

GDP

U.S. economic growth picked up in the third quarter of 2025, with real gross domestic product (GDP) increasing at an annualized rate of 4.3%, according to the initial estimate from the U.S. Bureau of Economic Analysis. This follows 3.8% growth in the second quarter, signaling continued momentum in the economy.

Due to the recent government shutdown, this initial third-quarter report replaces both the advance estimate originally scheduled for October 30 and the second estimate that had been planned for November 26.

The increase in real GDP during the third quarter was driven primarily by stronger consumer spending, higher exports, and increased government spending. These gains were partially offset by a decline in investment. Imports—which subtract from

GDP calculations—also decreased during the quarter. Compared to the second quarter, the faster pace of growth reflects a smaller decline in investment, an acceleration in consumer spending, and renewed growth in both exports and government spending. Imports continued to fall, though at a slower rate than in the prior quarter.

Jobs & Unemployment

U.S. job growth remained subdued in November, with nonfarm payrolls increasing by 64,000, following an estimated loss of 105,000 jobs in October tied largely to the federal government shutdown. While November’s gain exceeded economists’ expectations of roughly 40,000 jobs, overall employment has shown little net change since April.

Federal government employment continued to decline, down 6,000 in November after falling 162,000 in October, while gains were concentrated in health care and construction. Revisions also lowered prior job estimates for August and September.

The unemployment rate held at 4.6% in November, a four-year high, with 7.8 million people unemployed, up from 7.1 million a year earlier.

Data quality remains a key concern following the 43-day government shutdown, which disrupted October data collection.

Sources:

https://www.bls.gov/news.release/pdf/empsit.pdf

https://www.theguardian.com/business/2025/dec/16/jobs-report-october-november

Inflation

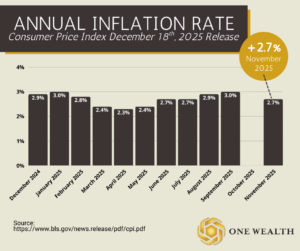

November inflation data showed continued moderation, with the Consumer Price Index (CPI) rising 2.7% over the past 12 months, according to the Bureau of Labor Statistics. That marked a slowdown from the prior 12-month pace of 3.0% ending in September.

Core inflation, which excludes food and energy, increased 2.6% year over year, reinforcing signs that broader price pressures are easing. On a monthly basis, both headline and core CPI rose 0.2%, below economists’ expectations of 0.3%.

Looking beneath the surface, energy prices rose 4.2% over the past year, while food prices increased 2.6%. Shelter costs, which account for roughly one-third of the CPI, rose 3% year over year, a significant development given shelter’s outsized role in driving inflation earlier in the cycle.

The November report was delayed and incomplete due to the federal government shutdown, which prevented data collection in October. As a result, economists caution against reading too much into a single report. Still, the cooler-than-expected inflation data has strengthened expectations that the Federal Reserve may have room to ease policy further in 2026, with markets increasing the probability of a March rate cut while January expectations remain low.

Sources:

https://www.bls.gov/news.release/cpi.nr0.htm

https://www.cnbc.com/2025/12/18/cpi-inflation-report-november-2025.html

Real Estate & Mortgage Market

Throughout 2025, the U.S. real estate and mortgage markets continued to operate under the weight of elevated interest rates and lingering affordability challenges. Mortgage rates spent much of the year in the mid-6% range after peaking above 7% earlier, keeping monthly payments meaningfully higher than the pre-2022 norm. While demand never disappeared, higher financing costs limited how many buyers could comfortably transact, resulting in lower overall sales volume rather than broad price declines.

Inventory showed modest year-over-year improvement, particularly in certain regions, but supply remained well below historical averages. A key factor was the ongoing “lock-in effect,” as many homeowners with sub-4% mortgages remained reluctant to sell. This dynamic helped keep home prices relatively resilient nationwide, even as buyers gained slightly more negotiating power in markets where new construction or local economic pressures increased supply.

On the mortgage side, purchase activity remained steady but subdued, while refinance demand proved highly rate-sensitive.

Brief dips in mortgage rates led to sharp but temporary increases in refinancing applications, illustrating how many households are waiting just above their break-even rate. Overall, 2025 was less about dramatic shifts and more about adaptation – buyers,

sellers, and lenders adjusting to a higher-rate environment that appears more structural than temporary.

Sources:

https://apnews.com/article/814329ffcabdd60470f390407778f644

https://www.nar.realtor/research-and-statistics

https://www.reuters.com/markets/us/

Notable Quote

“Volatility is not the same as risk.”

-Howard Marks