Stock Market

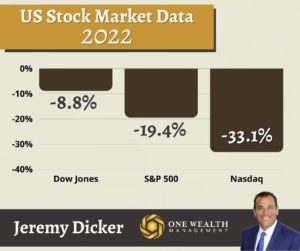

In 2022, the U.S. stock market experienced its worst year by percentage decline since the financial crash in 2008, snapping a three-year streak of Wall Street gains.

At the final bell of 2022, those three major benchmarks performed as follows for the year:

Dow Jones -8.8%

S&P 500 -19.4%

Nasdaq -33.1%

And for December, the three major indices performed as follows:

Dow Jones -4.2%

S&P 500 -5.9%

Nasdaq -8.7%

Inflation

The December 13 inflation report brought a sigh of relief, as the Consumer Price Index rose just 0.1% over the previous month, coming in significantly lower than forecasts.

Economists expected the CPI to rise 0.3% in the one month since the last report but falling energy prices kept inflation at bay.

Year-over-year, all-items inflation increased by 7.1%, also lower than the estimated 7.3% mark. That represents the smallest monthly increase since December 2021.

With two straight months of lower-than-expected inflation readings, the Fed will likely take this as a welcome sign that their rate-tightening campaign is slowing the U.S. economy and price growth.

Energy prices (- 1.6%) were the biggest contributor to decreasing inflation, thanks to a 2% decrease in gasoline costs and more. However, food prices rose 0.5% over the month. And shelter prices, which make up about one-third of weighted CPI, rose 0.6% for the month, now a concerning 7.1% higher than this time last year.

Core CPI (less food and energy) rose 0.2% for the month and 6% annually, both lower than the estimated 0.3% and 6.1% increases, respectively.

Interest Rates and the Fed

At their December 14th meeting, the Federal Reserve raised their benchmark interest rate by 0.50%, a predicted increase that was confirmed by the previous day’s report.

Still, a 0.50% increase comes in lower than the Fed’s previous four 0.75% rate hikes, their most aggressive campaign since the 1980s.

With the Central Bank’s Fed funds rate now at a range of 4.25%-4.5%, it’s reached the highest level since 2007.

Wall Street is pondering how the Fed will handle rate hikes in the near future. While a 0.50% increase does qualify as tapering, analysts don’t expect a pause to rising rates any time soon.

Forecasts now predict rates to peak at 5.1% in early 2023, which is 50 basis points higher than previous estimates back in September of this year.

That much has been confirmed by Fed Chairmen Jerome Powell. At the last Fed meeting, Powell said that rates would need to move higher than originally thought as inflation came in hotter than projected.

Economists generally agree on the Fed funds rate falling to 4.1% in 2024, as core inflation isn’t expected to settle near the Fed’s target rate of 2% until after 2023.

Jobs and Unemployment

Non-farm payrolls rose by 263,000 in November’s employment report by the U.S. Bureau of Labor Statistics (latest data). That left the unemployment rate unchanged from the previous month at 3.7%.

The latest jobs numbers are consistent with employment gains over the previous three months with an average of +282,000. For the year, monthly job growth has averaged +392,000 versus +562,000 average monthly job gains in 2021.

For the month, the largest job gains occurred in the sectors of leisure and hospitality (+88,000), health care (+45,000), and government (+42,000).

Meanwhile, employment fell in retail trade, transportation, and warehousing in November.

Also of note in the U.S. Labor release was a revision of October’s non-farm payrolls up 23,000 to +284,000, while September’s numbers were revised down by 46,000 to +269,000 for that month.

With Fed rate increases aiming to slow the economy, analysts expect the unemployment rate to rise to 4.6% sometime in 2023, remaining around that level through 2024.

The next employment report revealing December’s data is set to be released on Friday, January 6, 2023.

Gross Domestic Product

In the third quarter of 2022, the U.S. Gross Domestic Product increased at an annual pace of 3.2%. That upwardly revised number surpassed estimates of Q3 GDP (which came in at 2.9%) on the back of strong consumer spending.

That number looks robust compared to the negative 0.6% GDP drop we saw in Q2 of 2022.

However, analysts are fully expecting a slowdown when Q4 GDP data is released, as ripples from the Fed’s campaign to combat inflation continue to spread. A panel of experts anticipate the U.S. economy growing just 0.5% in 2023 before picking up steam to 1.6% GDP growth in 2024.

When asked for his reaction to these forecasts, Fed chairman Jerome Powell reiterated that slow GDP growth is still growth, and better than the specter of negative GDP dragging the U.S. economy into a recession.

“I don’t think it would qualify as a recession, because you’ve got positive [GDP] growth,” said Powell.

The advance estimate for Q4 2022 GDP is set to be released on January 26, 2023.

Mortgage and Housing

After spiking past 7% in the third quarter of 2022, mortgage rates settled in Q4, falling to a national average of 6.27% for a 30-year-fixed home loan, according to Freddie Mac.

The Federal Housing Finance Agency released their conforming loan limits for 2023, and they’re all the way up to $726,200 for one-unit properties across most of the country, an increase of $79,000 from 2022.

In counties designated as high-cost areas, the new conforming loan limit will be $1,089,300 in 2023. (Conforming loans are usually easier to obtain and come with better rates than home loans that don’t fit into that “box.”)

The housing market is experiencing a slowing. According to the National Association of Realtors, existing home sales fell another 7.7% in November (latest data), the tenth month in a row of slower sales volume.

In November, national home prices were up 3.5% year-over-year, with the existing home sale price at $370,700. In California. By the time 2022 concludes, forecasts place the California median home sale price up 5.2% for the year to a median home sale price of $834,400.

Notable Quote

“Money is only a tool. It will take you wherever you wish, but it will not replace you as the driver.”

-Ayn Rand