Stock Market

U.S. stocks surged on the final day of April 2026 with all three major indices closing at record highs, thanks to investors looking past lingering geopolitical concerns and a softer-than-expected GDP reading of 2% annualized growth for Q1 2026.

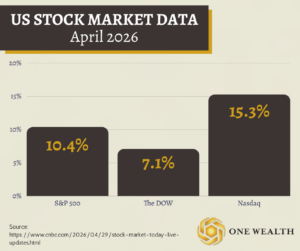

As a whole, April delivered an exceptional month for equities. For the month, the stock market’s three major indices performed as follows:

S&P 500 10.4%

The Dow 7.1%

Nasdaq 15.3%

It was the S&P’s best month since November 2020, the Nasdaq’s best month since April 2020, and the Dow’s strongest monthly advance since November 2024.

***

Source:

https://www.cnbc.com/2026/04/29/stock-market-today-live-updates.html

Inflation

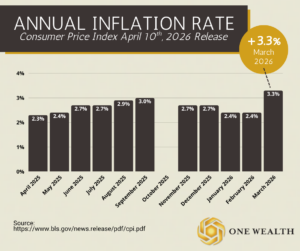

The Consumer Price Index (CPI) rose 0.9% in March, bringing the annual inflation rate to 3.3%, up from 2.4% in February and the highest level since April 2024.

The increase was largely driven by a sharp rise in energy prices, which surged 10.9% for the month and 12.5% over the past year. Gasoline alone jumped 21.2% in March, accounting for nearly three-quarters of the overall increase, largely tied to geopolitical tensions involving Iran. Shelter costs also continued to rise modestly, increasing 0.3% for the month and 3% annually.

Despite the headline increase, underlying inflation remained relatively contained. Core inflation, which excludes food and energy, rose just 0.2% in March and 2.6% over the past year – both slightly below expectations. Food prices were unchanged for the month and up 2.7% annually, with grocery prices declining 0.2%. There were also pockets of price declines in categories like medical care, personal care, and used vehicles, suggesting that broader inflation pressures remain more moderate beneath the surface.

Overall, March’s inflation spike appears largely driven by temporary energy-related factors rather than a broad-based acceleration in prices.

***

Sources:

https://www.bls.gov/news.release/cpi.nr0.htm

https://www.cnbc.com/2026/04/10/cpi-inflation-report-march-2026.html

Jobs & Unemployment

U.S. job growth rebounded in March, with nonfarm payrolls increasing by 178,000, marking the largest gain in 15 months and a sharp reversal from February’s revised decline of 133,000.

The unemployment rate edged down to 4.3%, though the drop was largely driven by 396,000 people exiting the labor force. Job gains were concentrated in health care, construction, and transportation/warehousing, while federal employment continued to decline.

Despite the headline strength, underlying trends suggest a more mixed picture. Economists caution that March data may not yet reflect emerging risks, particularly from geopolitical tensions such as the ongoing Iran conflict and policy uncertainty around tariffs. Overall, the labor market remains resilient on the surface, but with signs of cooling and potential headwinds ahead.

***

Sources:

https://www.bls.gov/news.release/pdf/empsit.pdf

https://www.reuters.com/world/us/us-employment-growth-rebounded-march-unemployment-rate-falls-43-2026-04-03/

The Fed and Rates

In its April meeting, the Federal Reserve left its benchmark interest rate unchanged in a target range of 5.25% to 5.50%, marking another pause as policymakers assess inflation and economic data. Officials noted that inflation remains above the Fed’s 2% target, with recent readings still running closer to the mid-2% to 3% range, while the labor market has stayed relatively strong.

The decision was not unanimous, reflecting differing views among policymakers on the path forward. The Fed emphasized that it needs more consistent evidence that inflation is moving sustainably lower before considering rate cuts, signaling that rates could remain at current levels for longer depending on upcoming economic data.

***

Source:

https://www.cnbc.com/2026/04/29/fed-meeting-today-live-updates-warsh-powell.html

GDP

U.S. economic growth slowed significantly in the fourth quarter of 2025, with real GDP increasing at an annual rate of 0.5 percent, down from both the prior estimate of 0.7 percent and a much stronger 4.4 percent pace in the third quarter.

The downward revision was driven primarily by a pullback in private inventory investment, particularly within wholesale trade, and was further impacted by the October 1 to November 12, 2025 federal government shutdown, which reduced growth by an estimated 1 percentage point and delayed key data collection. Despite these headwinds, growth was supported by consumer spending and investment, while declines in exports and government spending weighed on overall output. Imports decreased, which partially offset the drag on GDP.

Real gross domestic income (GDI) increased 2.6 percent, with the average of GDP and GDI rising 1.5 percent for the quarter. For the full year, real GDP grew 2.1 percent in 2025, down from 2.8 percent in 2024, reflecting a broader moderation in economic momentum.

***

Sources:

https://www.bea.gov/index.php/news/2026/gdp-third-estimate-industries-corporate-profits-state-gdp-and-state-personal-income-4th

https://qz.com/us-gdp-q4-2025-final-estimate-revised-down-040926

Real Estate & Mortgage Market

The U.S. housing market in April 2026 showed early signs of shifting toward a more buyer-friendly environment, driven by a meaningful combination of rising inventory and easing mortgage rates. Active listings and new listings both increased during the month, continuing a multi-year trend of inventory recovery and giving buyers more options than they’ve had in recent spring seasons. At the same time, price growth softened, with data showing declines on a price-per-square-foot basis and broader signs that home values are stabilizing after several years of elevated appreciation.

Mortgage rates were a central driver of market sentiment throughout April. After spiking earlier in the month, the average 30-year fixed rate moved lower, settling around the low-6% range (approximately 6.2%–6.3% by late April). This decline—while modest—helped improve affordability at the margin and led to a noticeable pickup in buyer activity, including increases in mortgage applications and renewed engagement from sidelined buyers.

Looking ahead, expectations for mortgage rates remain mixed. While some near-term relief has materialized, most forecasts suggest rates will stabilize around the mid-6% range through 2026, with only gradual declines possible unless inflation cools more meaningfully or the Federal Reserve shifts policy. As a result, the housing market is likely to continue rebalancing rather than rapidly accelerating—characterized by improving supply, moderating prices, and demand that responds quickly to even small movements in interest rates.

***

Sources:

https://www.realtor.com/news/real-estate-news/mortgage-inventory-weekly-housing-market-update-april-24-2026/

https://finance.yahoo.com/personal-finance/mortgages/article/when-will-mortgage-rates-go-down-april-23-2026-190610167.html

Notable Quote

“You can’t predict. You can prepare.”

-Howard Marks