Stock Market

April closed a volatile month with a rebound despite weaker than anticipated economic growth numbers, although the S&P 500 and Dow still ended the month down while the tech-heavy Nasdaq eked out a slight gain.

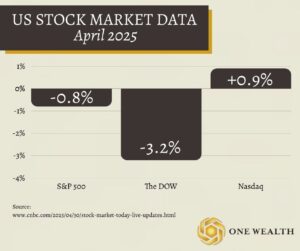

For the month, the stock market’s three major indices performed as follows:

S&P 500 -0.8%

The DOW -3.2%

Nasdaq +0.9%

Source: https://www.cnbc.com/2025/04/30/stock-market-today-live-updates.html

GDP

The U.S. economy unexpectedly shrank in the first quarter of 2025, marking the first contraction in three years. According to the Bureau of Economic Analysis, GDP declined at an annualized rate of 0.3%, a sharper drop than the 0.2% economists had forecast and a notable reversal from the 2.4% growth seen in Q4 2024. This slowdown was largely due to a 41.3% surge in imports, as businesses rushed to stock up ahead of anticipated tariff increases from the Trump administration. Since imports count as a negative in GDP calculations, this surge alone subtracted roughly 5 percentage points from economic growth.

Despite the headline contraction, underlying economic activity remained relatively strong. Consumer spending and domestic sales both showed resilience, with final sales to domestic purchasers rising 3%. Core inflation, as measured by the Personal Consumption Expenditures index, came in hotter than expected at 3.5%. Economists suggest that while the GDP decline is notable, it does not signal a recession—rather, it reflects temporary trade-related distortions ahead of policy changes that took effect in April.

Jobs & Employment

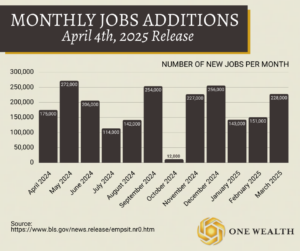

The U.S. labor market showed solid momentum in March, with nonfarm payrolls rising by 228,000—well above the revised February total of 117,000 and surpassing the Dow Jones forecast of 140,000, according to the Bureau of Labor Statistics.

Healthcare continued to lead job creation, adding 54,000 positions—right on pace with its 12-month average and consistent with trends seen in previous months.

Despite the strong job gains, the unemployment rate edged higher to 4.2%, slightly above the projected 4.1%, as more Americans entered the labor force.

While the report offers reassurance about the labor market’s stability, it comes amid broader economic uncertainty. President Trump’s recent tariff announcement has stirred concerns about a potential global trade war and its implications for future growth.

Source: https://www.cnbc.com/2025/04/04/jobs-report-march-2025-.html

Inflation

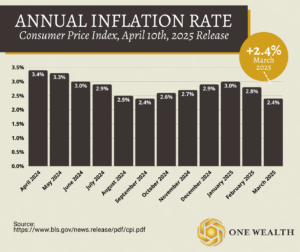

The latest Consumer Price Index (CPI) report shows a slight decline in inflation for March. According to the U.S. Bureau of Labor Statistics, the CPI for All Urban Consumers (CPI-U) decreased by 0.1% on a seasonally adjusted basis—marking a shift from the 0.2% increase recorded in February. Over the past 12 months, consumer prices rose 2.4% before seasonal adjustment.

Energy prices saw a notable drop, falling 2.4% in March. This was largely driven by a 6.3% decline in gasoline prices, which more than offset modest increases in electricity and natural gas costs.

Food prices, however, continued to climb, increasing 0.4% in March. Grocery prices (food at home) rose by 0.5%, while dining out (food away from home) edged up 0.4%.

When excluding food and energy—often referred to as core inflation—the index rose 0.1% in March, following a 0.2% rise in February. Categories seeing upward price pressure included personal care, medical care, education, apparel, and new vehicles. Meanwhile, prices declined for airline fares, used cars and trucks, recreation, and motor vehicle insurance.

This data suggests inflationary pressures are continuing to moderate, which could influence the Federal Reserve’s next moves on interest rates and monetary policy.

Source: https://www.bls.gov/news.release/cpi.nr0.htm

The $35 Trillion Problem.

The growing U.S. national debt, now at $35 trillion, presents complex challenges. While the debt level is high, and interest payments are consuming a larger share of the federal budget, the immediate impact on investor confidence remains muted.

The debt-to-GDP ratio—currently at 121%—is a more critical measure of fiscal health than the total debt alone. A ratio above 100% signals that the country owes more than it produces annually, raising concerns about future borrowing, interest costs, and fiscal flexibility. Rising interest payments, now over $1 trillion a year, further strain the budget, potentially crowding out spending on infrastructure, education, and other priorities.

Without significant policy changes—such as tax increases or spending cuts—the debt burden could continue to grow, possibly leading to higher taxes, reduced public services, and constraints on future economic growth.

The future of U.S. debt management will hinge on political will, economic conditions, and fiscal discipline in the years ahead.

Source: https://www.crystalfunds.com/insights/us-national-debt-how-much-is-too-much-for-us-economy

Real Estate and Mortgage

Home loan rates remained elevated last month as consumer and investor confidence faltered amid new White House tariffs. Freddie Mac reported that the average 30-year fixed mortgage rate was 6.81% for the week ending April 24, down slightly from 6.83% the previous week — which had marked the biggest one-week jump since last August.

Overall, rates in the high 6% range have contributed to a slump in mortgage applications for two consecutive weeks, according to the Mortgage Bankers Association (MBA). With rates hovering near 7%, many potential buyers are holding off until there’s more clarity.

The housing market is feeling the effects: The National Association of Realtors (NAR) reported that sales of previously-owned homes fell to an annual pace of 4.02 million in March, a sharp drop that points to 2024 potentially being the worst year for home sales since 1995. Redfin also noted that homes are taking longer to sell and receiving fewer bids — the slowest pace since 2019 — as supply climbs and demand softens.

Notable Quote

“Markets are never wrong; opinions often are.”

-Jesse Livermore